Mid-market companies have moved past the AI adoption problem and are now into the AI value problem. The tools are already in the building, the licenses are already paid, and the bottom line has still not moved. The reasons are well documented now, and the companies closing that gap follow a clear pattern.

In fact the conversation has been stuck on the wrong question, either replace or resist or automate or fall behind. The data from this year tells a more useful story, and it starts with what is actually happening inside companies right now.

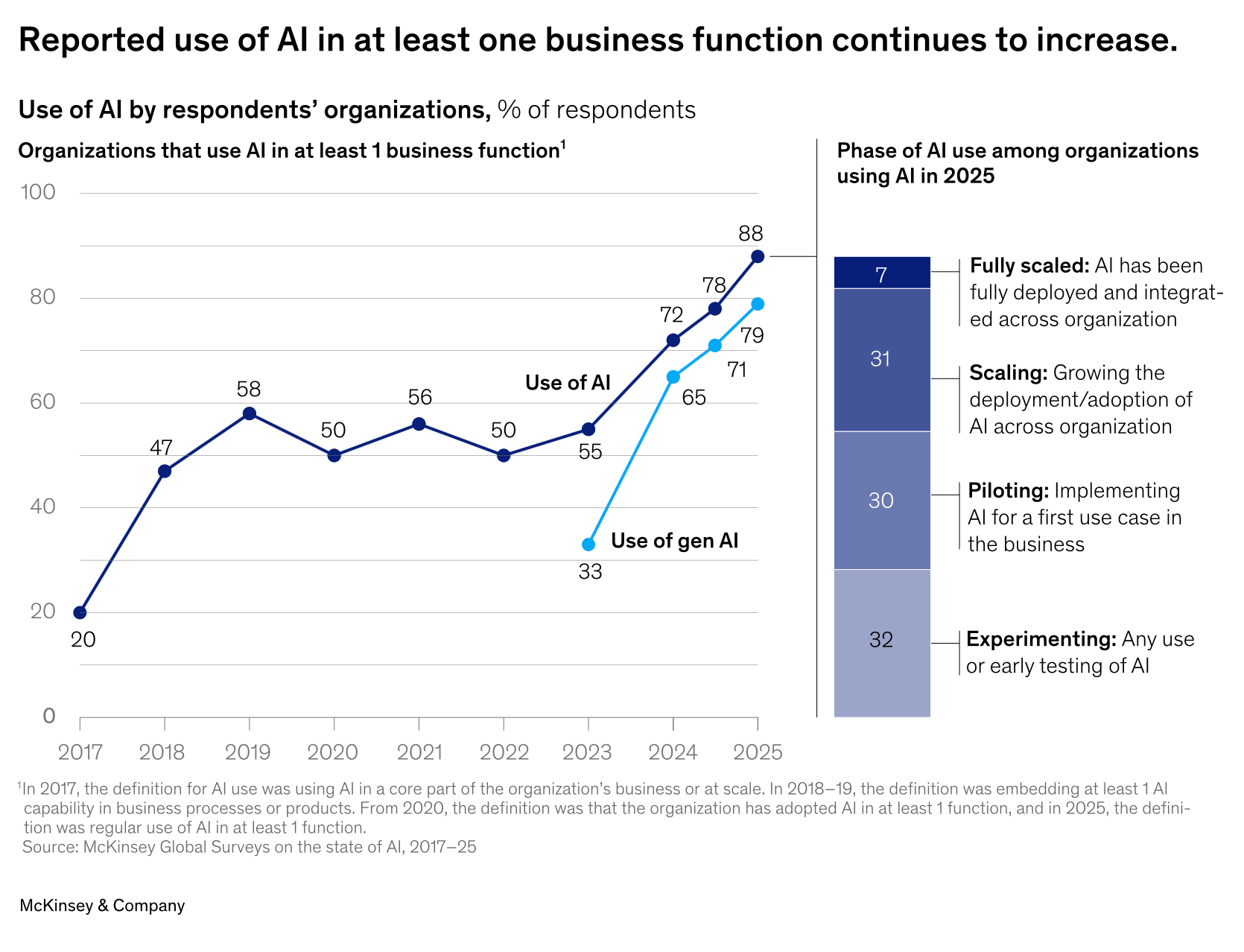

Where mid-market companies actually stand

Walk into any 100-person company today and the scene is the same. Sales reps draft emails with ChatGPT. Finance runs Copilot for variance commentary. Operations has a chatbot somewhere. Marketing tests image generation. The tools are already in the building.

According to McKinsey's State of AI 2025 survey of 1,993 companies across 105 countries, 88% of organizations regularly use AI in at least one business function (source). BCG's AI at Work 2025 survey of over 10,600 workers across 11 countries put regular use at 72%, with leaders and managers above 75% and frontline workers stuck at 51% (source).

And yet, the financial impact is missing. McKinsey reports that only 39% of organizations see EBIT impact at the enterprise level, and nearly two-thirds have not begun scaling AI beyond pilots. MIT's NANDA initiative ran a study published in 2025 covering 150 executive interviews, 350 employee surveys, and 300 public AI deployments, and found that 95% of enterprise generative AI pilots produced no measurable P&L impact, against an estimated $30-40 billion in enterprise spend (source via Fortune).

So the operational problem is no longer access to AI. The problem is that AI is in the building but the business has not changed.

The default playbook every COO recognizes

The reflex move follows the same sequence in nearly every mid-market company. License Copilot or ChatGPT Enterprise. Add a vertical SaaS with an AI module. Launch a pilot in one department. Set up an AI committee. Measure hours saved per task. Report a productivity number to the board.

The framing under all of this is cost. How many hours will this remove. How many FTEs can we redeploy. How fast can we shrink the support team. ROI gets modeled as labor subtraction, and the metric of success is time removed from a spreadsheet.

When the bottom line does not move, the second instinct is to scale the same approach. More licenses, more pilots, a consultant to lead the transformation, possibly a new platform. The shape of the spend changes. The shape of the work does not.

McKinsey Global Institute documented this pattern in January 2026: 90% of companies invest in AI, and fewer than 40% report meaningful bottom-line impact (source). The gap is not technological. It is structural.

Why this stops working at the second pilot

Three reasons, all uncomfortable for finance, IT, and operations to hear in the same room.

The ROI model is measuring the wrong thing. Time saved is not value created. If a customer success team saves 10 hours a week and uses those hours to send more of the same generic follow-ups, the company gets nothing. ROI from AI shows up in time-to-decision, error reduction, customer impact, and revenue per employee, and almost never in hours subtracted from a timesheet.

Tools layered on broken processes amplify the existing dysfunction. Adding a chatbot to a workflow built for a pre-AI world produces incremental noise on top of a process that was already fragile. McKinsey's 2025 data is direct on this point: high performers are nearly three times more likely to have fundamentally redesigned workflows end-to-end, and that single variable correlates more strongly with EBIT impact than any other factor tested.

The human side gets treated as an afterthought. AI lands on teams without context, without training, and without a clear new operating model. The employees who already use AI personally accelerate. The rest disengage, which is exactly what BCG documented in the frontline adoption gap. Two parallel speeds inside the same company create more friction than no AI at all.

There is also a credible counter-position worth naming directly. Some economists argue AI is producing net labor displacement, not augmentation. Goldman Sachs Research estimated in April 2026 that AI has reduced US monthly payroll growth by roughly 16,000 jobs over the past year and lifted unemployment by 0.1 percentage point (source). That is real. Tier-one support, basic copywriting, junior analyst work, and entry-level coding are getting compressed. The same Goldman analysis found that occupations with strong augmentation potential gained roughly 9,000 jobs per month. AI replaces tasks. What leadership does with the freed capacity decides whether teams are empowered or hollowed out.

Designing for capacity

The shift that separates AI high performers from the other 94% is not bigger budgets or better models. It is treating AI as an operating model change.

McKinsey Global Institute estimates that AI agents and robots could unlock around $2.9 trillion in annual economic value in the US alone by 2030, and the same research is clear that this value materializes only when organizations redesign work around human-AI partnerships rather than automating tasks in isolation. PwC's May 2026 TBR Talks reached the same conclusion from a different angle: across industries, full automation rarely produces durable competitive advantage, and the companies pulling ahead are those designing AI to support decisions rather than execute them (source).

What changes in practice looks like this.

Capacity becomes the asset, not cost reduction. The question shifts from "how much did we save" to "what did this team have time to do that it could not before." Deeper account analysis. Better customer follow-up. Faster product iteration. Strategic conversations instead of admin. Cost reduction becomes a byproduct of better work, rather than the headline.

Workflow redesign replaces task automation. Picking one end-to-end process and mapping where AI executes routine cognitive work, where it assists human judgment, and where humans must own the decision changes the sequence of the work itself. This is where the EBIT impact lives, and the McKinsey data confirms it as the single strongest predictor of value capture.

Team transformation replaces individual productivity. Meetings shrink because pre-reads are AI-summarized. Decisions accelerate because options are pre-analyzed. Onboarding compresses because institutional knowledge becomes queryable. The shift is not "we use AI." It is "we work faster, with more evidence, and with less friction between roles." Habits change first. Culture follows.

Customer impact replaces internal efficiency as the headline. AI gets sold to the team as a way to remove waiting time, fragility, and rework from the processes that touch the customer. Cycle times drop. Quality rises. Customers notice. Revenue follows. The internal story becomes one of capability, not subtraction.

This reframing changes how AI gets funded, sponsored, and measured. It also changes who owns it. AI stops being a CIO project only and becomes a COO and CEO accountability.

What to do this quarter

Six steps, in order. None of them require a new platform.

- Pick one process with measurable customer impact. Sales-to-cash, ticket resolution, proposal generation, monthly close. Resist the urge to do AI everywhere. Concentration beats sprawl.

- Map the process before touching any tool. Document who does what, in what order, with which inputs and waiting times. BPMN, swim lanes, whatever the team understands. The work that has not been seen cannot be redesigned.

- Classify each task into three layers: full AI execution, human-AI collaboration, and human-only judgment. Most teams misclassify on the first pass and put too much in the first bucket. Be conservative.

- Redesign the workflow on paper first. Tools come after the design and serve the new sequence, not before it.

- Decide where the freed capacity goes before you free it. If the rollout creates 15 hours per analyst per week, document the redeployment upfront. Without that step, the capacity evaporates into more email and the ROI argument collapses.

- Measure outcomes, not activity. Track time-to-delivery, first-time-right rate, customer NPS movement, revenue per FTE, and decision cycle time. Track usage too, and never as the headline metric. Activity flatters pilots and hides failure.

Two things worth saying out loud to the team during the rollout. Some tasks will disappear, and the new responsibilities that replace them will be named. AI is not an IT project, it is an operating model change, and it is owned by operations and the CEO. Trust collapses fast when leaders sell empowerment while quietly planning cuts, and the most direct way to prevent that collapse is to be specific about both sides of the equation upfront.

What this leaves you with

AI is not the transformation. The decision to redesign how the business runs around AI is the transformation. The technology is the catalyst, not the strategy.

The companies that pull ahead in the next 24 months will not be the ones with the loudest AI announcements or the largest license counts. They will be the ones quietly rewiring their workflows, redirecting freed time toward higher-value work, and changing how teams collaborate around data and decisions. Five takeaways are worth keeping in front of the leadership team.

- AI replaces tasks. Companies decide whether it replaces teams.

- ROI is capacity unlocked, time-to-decision compressed, and customer impact increased. Hours saved is the side effect.

- Workflow redesign is the single strongest predictor of EBIT impact from AI. Tools without redesign produce noise.

- The transformation is cultural before it is technical. New habits, new collaboration patterns, new decision rhythms.

- Direct, honest communication with the team beats motivational AI slogans every time.

The DNA of the company does not change. The way the company works together does. That is the actual shift.

Questions leaders are actually asking

Will AI take my team's jobs ?

It will take specific tasks. Whether it takes jobs depends entirely on how leadership redeploys the freed capacity. Companies that use AI to compress headcount get short-term margin and long-term capability loss. Companies that redirect humans toward judgment, customer impact, and strategy build durable advantage. Goldman Sachs Research found both effects active in the same economy right now, with augmentation-heavy roles gaining employment while substitution-heavy roles lose it.

How long before we see real ROI ?

Tool-level ROI (hours saved) shows up in weeks. Workflow-level ROI (cycle time, customer impact) shows up in 3 to 6 months. Business-level ROI (EBIT, revenue per FTE) shows up in 12 to 24 months. Any AI program selling 30-day transformation is selling a pilot, not a result.

Do we need to hire AI specialists ?

A small core team helps. Most of the work is process redesign and change management, not machine learning. The biggest skill gap in mid-market companies is process literacy and decision discipline, and McKinsey's data shows demand for AI fluency has grown nearly sevenfold in two years across non-technical functions.

What about teams losing critical thinking through AI over-reliance ?

Real and rising. Build human validation steps into workflows where outputs matter, treat critical thinking as a muscle that needs use, and resist the temptation to remove human review from every step that AI can handle technically. The cost of atrophy compounds quietly and shows up in decision quality two years later.

What is the single biggest mistake mid-market companies make with AI ?

Buying tools before mapping processes. The second biggest is selling AI internally as cost reduction. The first wastes money. The second destroys trust.

Where do we start if we have done nothing yet ?

Pick one process that touches the customer and runs at least weekly. Map it. Identify the three biggest waiting points or rework loops. Test one AI-assisted redesign on that specific friction. Measure outcomes, not activity. Expand from there.

Sources: McKinsey State of AI 2025 (link) · McKinsey Global Institute, January 2026 (link) · BCG AI at Work 2025 (link) · MIT NANDA GenAI Divide report via Fortune (link) · Goldman Sachs Research, April 2026 (link) · PwC, May 2026 (link)